(Source: Apple)

Overview

Apple (NASDAQ:AAPL) made a few key announcements on Monday (March 25) at the Show Time event, along with the most anticipated announcement regarding the launch date of the all-new streaming service: Apple TV+. However, the spotlight was quickly stolen from Apple TV+ by the revolutionary announcement of the Apple Card. Investors, analysts, and users have all been paying close attention to Apple Pay over many years, but the introduction of the Apple Card came as a surprise for many stakeholders, and I believe the prospects of this new development should be analyzed to assess whether the company stands to gain from this new development.

What is Apple Card?

I have to say, the introductory film about Apple Card on the company website is not only appealing but is promising. Investors should not get carried away by this though, and should try to see the bigger picture behind the Apple Card and how this product will impact earnings in future periods.

Apple Card is a revolutionary credit card developed by Apple in partnership with Goldman Sachs (GS)). Unlike a traditional credit card, the Apple Card is intended to serve more like a virtual credit card in collaboration with Apple Pay. However, there is a physical card as well; a titanium card without numbers, which a customer could use at any store that doesn’t accept Apple Pay.

Apple Card design

(Source: The Verge)

There are a few interesting features of the Apple Card, which require special attention in this analysis.

Who can obtain an Apple Card?

Subject to credit approval, any Apple user in the U.S. would be able to obtain the Apple Card, and I expect the company to roll out the card internationally by partnering with global banks, depending on the success of the Apple Card in the U.S. Considering the popularity and familiarity of credit cards in the U.S., failure to gain traction in the U.S. will automatically shut down any plans Apple might have to roll out this on an international basis.

What are the fees?

Apple claims the card would have zero fees, meaning there won’t be annual fees, cash advance fees, over limit fees, and not even late payment fees. Consumers might be thrilled at the idea of having to pay no fees for a stunning credit card, but in reality, there would indeed be late payment fees in the form of additional interest levied on the remaining balance. Even then, the total amount of fees owed to Apple would be drastically lower than to a traditional credit card issuer, and this should make Apple Card attractive to consumers.

As per available information at present, the Annual Percentage Rate (APR) charged by Apple would be around 13.24-24.24%, based on the creditworthiness of the customer. These rates might change as and when the company brings the Apple Card into the market in this summer.

In any case, it seems as if the median APR charged by Apple would be in line with the average APR for credit cards in the U.S.

Average APR for credit cards in the U.S.

{kind=link}

(Source: Credit Cards)

Is there a rewards program?

Yes, there is, and unlike many traditional credit card issuers, Apple provides these rewards as hard cash directly to the Apple Cash account or to the Apple Card as a chargeback, and all these rewards will be disbursed on a per transaction basis instantly. The company is certainly trying to add a touch of innovation here, and the increased popularity of rewards among consumers will position Apple Card as a favorite among rewards shoppers.

How to contact Apple the credit card company?

We all know how to contact Apple, but contacting the company for a matter related to the Apple Card is even easier, as this can be done by simply sending an iMessage on the in-built platform. This will add a layer of convenience to consumers, and considering how consumers have preferred to pay premium prices to acquire products and services that provide an additional level of convenience, I believe Apple Card would be embraced by consumers when released this summer.

What are some additional features of the Apple Card?

Apple Card will be built into the Apple Pay app, and the app will provide a streamlined experience to customers. Users of the Apple Card would be able to use the Apple Wallet app to see how much needs to be paid to avoid interest, the relevant due date for the minimum payment, the total amount spent on the card categorized into various segments, and rewards earned as well.

How will the introduction of Apple Card affect future earnings?

Apple is certainly focusing on existing customers to drive future earnings of the company, and the introduction of the Apple Card can be seen as another growth measure relying on the existing customer base of the company.

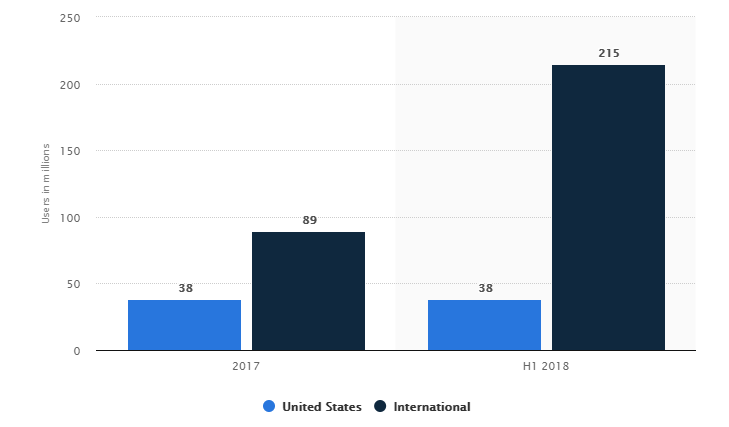

Over the years, the number of Apple Pay users has grown exponentially, and this provides a readily available market for the company to market its credit card.

Number of Apple Pay users in the U.S. as of mid-2018

{kind=link}

(Source: Statista)

With over 38 million users and growing, Apple Pay is certainly one of the most popular digital wallets in the U.S., and I believe Apple is tapping the right market to gain exposure to the financial sector. Digital wallets have grown in popularity over the last several years, and the growth of e-commerce and gig economy has certainly helped Apple Pay gain traction quickly.

From a macro perspective, the rise of digital-only banking services will provide tailwinds for Apple Card, and the massive brand loyalty associated with Apple, coupled with the possibility of attractive deals in the early days of the card, will provide a reason for consumers to consider signing up for an Apple Card.

I believe there are a few ways Apple can benefit by introducing the Apple Card.

First, the company will be adding a new stream of revenue from the credit card segment through interest received from consumers. The number of non-cash transactions is growing at a stellar rate on a global basis, and the North American non-cash transactions value is expected to reach $212 billion by 2021. This presents a robust growth opportunity for credit card issuers and other types of non-cash payment service providers, and Apple stands to gain through its existing Apple Pay service and the newly announced Apple Card.

{kind=link}

(Source: Capgemini/BNP Paribas)

The total addressable market is massive for Apple, and I believe the company will make inroads into this growing sector momentarily. Investors should never leave out the competition coming from existing players, but Apple has already laid the foundation with the success of Apple Pay.

There are a few assumptions an investor should make when trying to estimate how much in revenue the new Apple Card will bring in to the company. These include:

- Number of Apple iPhone users in the U.S. by the end of next 5 years

- Number of Apple Pay users

- Number of Apple Pay users who sign up for Apple Card

- APR charged for Apple Card

- Calculating Apple’s share of revenue.

Trefis has updated a model which investors can use to estimate the revenue generated by Apple Card by 2022, and their base-case scenario points to more than $1 billion in revenue from the Apple Card by 2022.

I believe building a model at this point involves a lot of uncertainties, as limited data is available on this product at present. Nonetheless, I believe Apple will make solid progress by acquiring a new customer base for the Apple Card, but retaining this customer base will be the real challenge for the company, as this involves a better understanding about consumer credit behavior and providing timely offers to keep users engaged.

This is just one way how the company would benefit from the introduction of Apple Card. I believe Apple will provide attractive offers to upgrade to the latest iPhone models using the Apple Card, and this should provide some momentum to iPhone sales in the future, though not significant. The company can generate a healthy revenue stream by introducing offers related to other Apple services such as Apple Music and Apple TV+ when they sign up with Apple Cards.

Finally, the introduction of the Apple Card will further enhance the company’s ecosystem and will result in higher user retention within the ecosystem. The company has time and time again emphasized its strategy of focusing on existing Apple users, and the all-new Apple Card is just another product that should build switching costs and help the company build on its loyal customer base. A higher loyal customer base will provide even more opportunities for Apple to introduce a wide variety of products and services to monetize the installed base even further.

Apple’s recently implemented pricing strategy continues to attract a high-spending customer base as well, which should provide a boost to the expected revenue from the credit card segment.

I believe Apple Card is just the start for Apple in the financial sector, and the company will probably introduce more products and services in the future to penetrate into this sector more. Only time will tell whether it would be successful in this segment, but from the outset, I clearly see growth opportunities.

In the short term, I expect Apple revenues to receive a small boost from interest income. However, I do not believe that the collected interest income would account for something substantial considering the company’s size. In any case, it would take a while for the Apple Card to gain traction in a competitive marketplace. However, the long-term outlook is much brighter for Apple, as the company can earn a meaningful revenue in the range of a few billion dollars from the Apple Card, and more importantly, the Apple Card will help the company build on its intangible assets.

This is how I believe the Apple Card will add the biggest value to the company. While I don’t expect earnings to materially be impacted by revenue earned from the issuance of Apple Card, I expect the release of the card to add intangible value to the Apple ecosystem, and it should help Apple build competitive advantages over its peers. In the long term, incremental revenue of a few billion dollars should provide a small boost to earnings per share, but the Apple Card might be helpful in bringing down the length of the replacement cycle of Apple devices if attractive discounts are offered to Apple Card users.

If Apple rolls out the Apple Card on an international basis anytime soon and focuses on providing other financial services such as peer-to-peer transactions, online only banking facilities, or even robot-advisory facilities, the company stands to earn billions of dollars in revenue considering the growth of these segments. However, it would take a long time for Apple to roll out such services, and the introduction of the Apple Card might well be the first step in becoming a financial services giant. In this light, I look at Apple Card more like a smaller step in a long journey rather than a product that will become a sensation and take the company to the next level.

At the current market price of $190, investors should be cautious about investing in Apple. Considering the latest services rolled out by Apple will take time to gain traction, and the decline in iPhone unit sales, I believe investors would be better off waiting for a higher margin of safety to invest in the company.

It is currently trading close to the consensus average estimate by analysts.

{kind=link}

(Source: TipRanks)

Investors with a very long time horizon should find a very attractive bet even at the current market price, but I recommend holding Apple at the current market price and waiting for a better entry point.

Where can Apple go wrong with the Apple Card?

Whether we like it or not, Apple is not a financial company but a tech company. It has a long way to go before establishing itself as a company that can identify consumer spending behavior and optimal pricing strategies for products and services offered. The existing marketplace is crowded with seasoned players who have built a reputation for credit card-related products for decades, and Apple as a newcomer will find it challenging to build a loyal customer base. In any case, it might take a while to build a loyal customer base, as this depends on a number of variables.

Having Goldman Sachs as a partner might ease some worries of investors, but then again, Goldman Sachs is not a seasoned player in the credit card industry by any means.

A failure in the credit card segment, however, will not result in severe financial losses for the company but would rather result in lower-than-expected earnings growth rates in the future.

Is Apple focusing on too many things too early?

Worldwide iPhone unit sales are declining, and Apple is working on becoming a services giant. It is focusing on a number of new products and services including healthcare, streaming, credit cards, and other subscription services such as Apple Music. One might feel the company is in a rush to find a solution to the declining unit sales, but I believe Apple is well within its limits in its search for the next billion-dollar revenue stream.

Apple has been working on these new products and services for a few years now, and it’s the right time for the company to make some moves before it’s too late.

Conclusion

The success of the Apple Card will depend on a number of variables, but in any case, I believe this all-new product will positively impact earnings in the next 5 years. Apple can certainly work on introducing the credit card on a global basis, and considering the bulk of Apple Pay users are located outside the U.S., this should provide a robust growth opportunity for the company. Once again, it’s not only about how much money the company can make from this product, but rather about the overall value it adds to existing Apple users.

Disclosure: I am/we are long AAPL. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.