I last discussed AMD (NASDAQ:AMD) as my top tech pick for 2018 roughly a year and a half ago. In early 2019, I wrote another article where I recommended holding on to your position. Since this past article, on January 2, the company’s stock has gone up by almost another 50%. Going forward, I expect AMD’s best years to continue to be ahead of it, as the company continues to innovate and improve its financials.

{kind=link}

Strategy

AMD has a strong heritage as a chip company, on the same level as Intel (NASDAQ:INTC) and Nvidia (NASDAQ:NVDA).

{kind=link}

AMD History – Investor Presentation

As can be seen the time period between 2011 and 2016, when the company had no major developments, minus expanding itself in game consoles, is when its stock price languished versus its peers. Since then, the company has created cheaper graphics cards, leapfrogged ahead of Intel in transistor size, and more impressive processors. This shows AMD’s impressive improvements.

The company plans to focus on a three-pronged strategy. First, it plans to continue its split GPU dominance with Nvidia. That means the company will need to continue to focus on gaming, computing, and VR. Next, the company plans to focus on data centers. Here, Intel and Nvidia by far dominate the entire industry. That means any market share AMD takes results in growth.

Lastly, the company plans to continue focusing on semi-custom platforms and partnerships. AMD expects that these will result in long-term growth, using its unique expertise.

AMD Technology Leading Edge

On top of AMD’s strategy, the company’s technology is leading edge.

{kind=link}

AMD 7nm Technology – Investor Presentation

AMD is the first of the major chip makers to reach 7 nm technology, ahead of both Nvidia and Intel. While Nvidia does have higher performance per watt at each process node, by shrinking faster, AMD has managed to remain more competitive. From a CPU perspective, on a dollar-to-dollar ratio, AMD blows Intel out of the water. As a result, AMD is now building the overall best processors in the world.

One of the largest developments here, to help cement AMD’s lead over Intel, will be the development of third-generation Ryzen processors to be released mid-year. These processors should result in continued performance leads by AMD. Among my peers building their own desktops, AMD processors are slowly being considered on the same level or better than Intel and being used in builds.

As a result of these developments, AMD expects total Ryzen systems to expand by 30% in 2019. This expansion should help its long-term earnings.

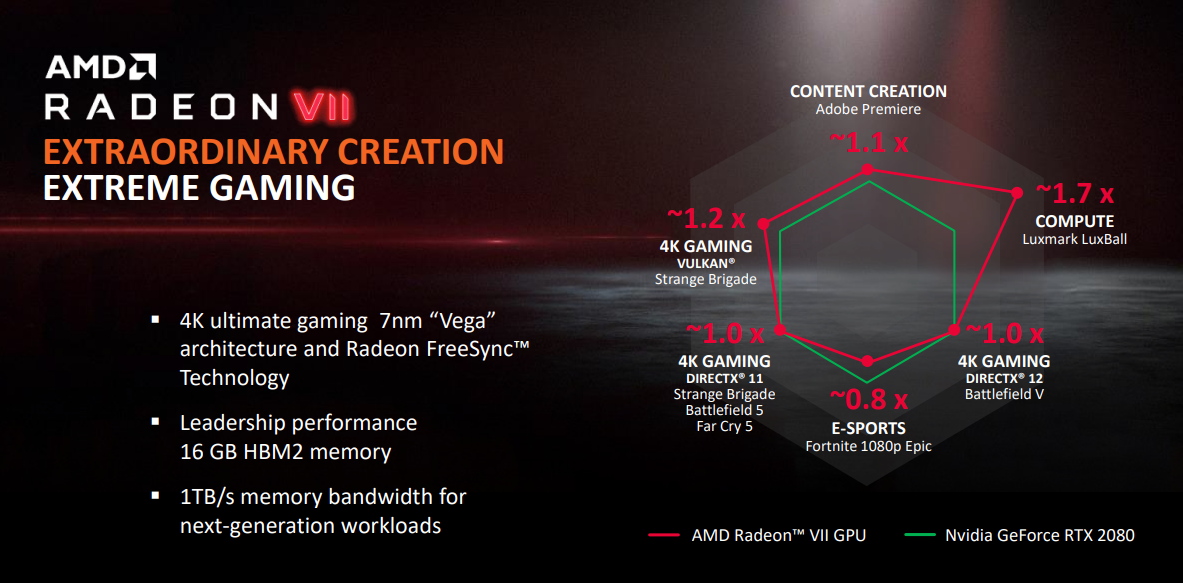

{kind=link}

AMD vs. Nvidia – Investor Presentation

AMD is continuing to work on its 7 nm VEGA GPUs, while continuing to move towards 7 nm “Navi” GPUs and 7+ nm “Next-gen GPUs”. As can see above, the company still isn’t, across the board, on the same level as Nvidia. One more thing AMD has to do at this point is compete with Nvidia on a software level. A significant portion of the best software for AI for example, such as TensorFlow, works best with Nvidia.

More so, something AMD has to worry about is that unlike Intel, Nvidia has continued to stay up to date and ahead of AMD. Even AMD’s Radeon 7, expected to be the answer to the Nvidia 2080 at a $100 lower price point, is considered to be somewhere in between the Nvidia 2070 and the 2080, i.e. it’s fairly priced, if not a bit overpriced. And AMD has still been unable to make a top-end graphics card that defeats Nvidia’s top end regardless of price.

Now to be fair, AMD has yet to release its Navi architecture, which is expected to be an improvement on the existing 7 nm process; however, given that Nvidia hasn’t yet made the movement down to a lower process, it seems likely, at least in the immediate future, that Nvidia will continue to be the preferred option for high-end, dedicated graphics cards.

Data Center Opportunity

Data centers are another enormous aspect of opportunity for AMD. This is especially true given that AMD effectively has a 0% stake in the data center markets.

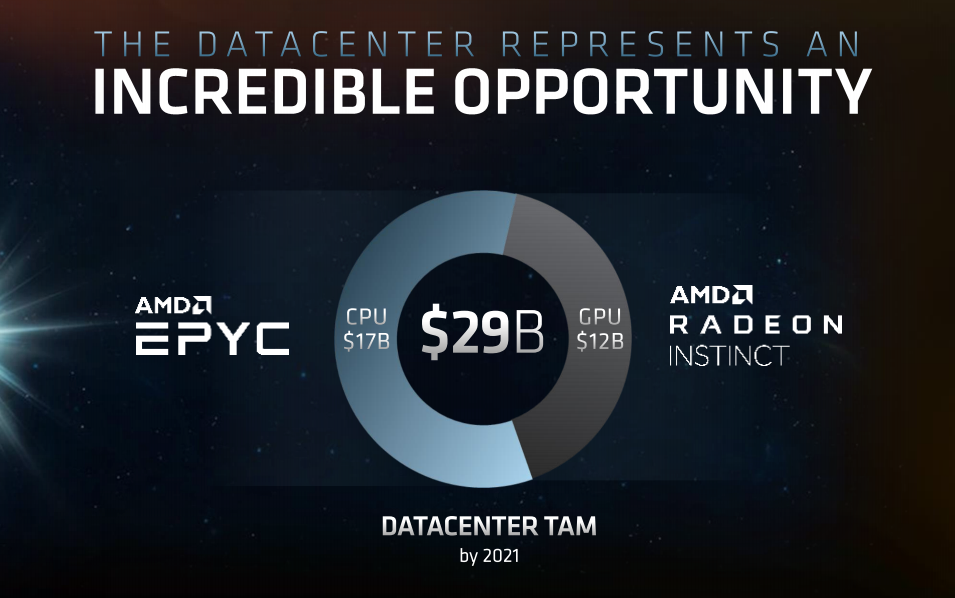

{kind=link}

AMD Datacenter – Investor Presentation

The data center markets are a $29 billion industry by 2021. Out of this, $17 billion is from EPYC CPUs and $12 billion from Radeon Instinct GPUs. I expect, especially in this CPU segment, that AMD has enormous potential.

AMD’s EPYC CPU is expected to provide up to 2x the performance per socket of the previous generation CPUs. At the same time, this is expected to expand to 4x the floating point performance per socket. At the same time, the sockets are compatible with the previous generation. This means that AMD’s EPYC CPUs are leading edge, and impressive.

Among these, is the “Rome” EPYC CPUs being launched in 2019. The processor consists of two 7nm CPUs along with a 14nm I/O die, well ahead of what Intel is currently producing at this time. This next generation, with massive improvements, should bring significant dominance over Intel. In fact, the improvement is so much, Intel’s CEO has publicly stated its interest to keep AMD’s market share low.

In fact, just six months ago, AMD’s market share in Europe had increased to 65% for desktop CPUs. This shows how AMD has leapfrogged over Intel in the CPU market, which should result in a significant increase in long-term revenue.

Financials

Now let’s discuss the last aspect of AMD’s growth, the company’s financials.

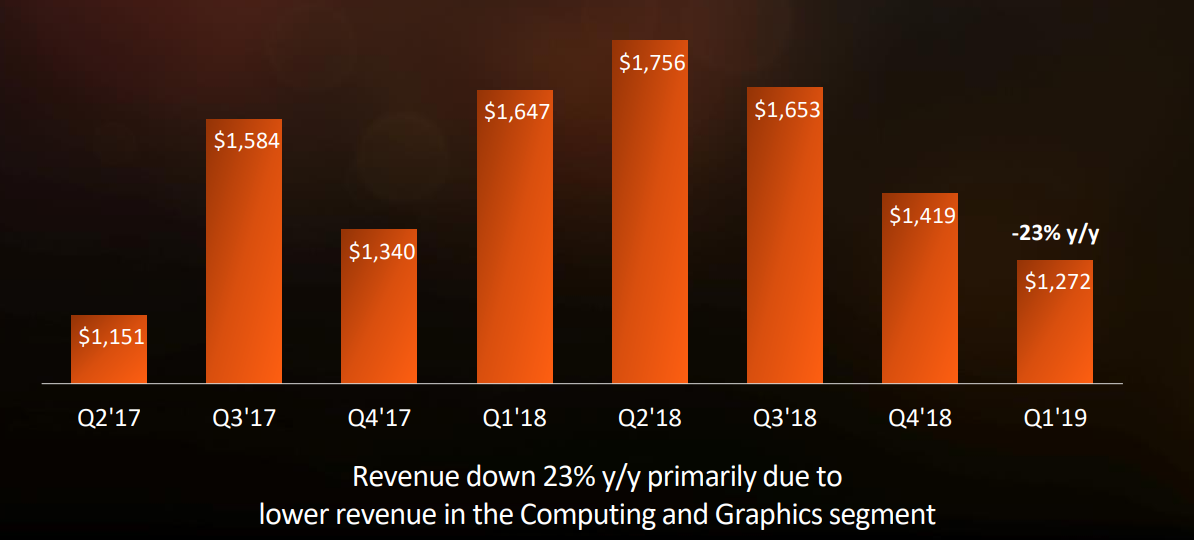

{kind=link}

AMD Revenue – Investor Presentation

This shows AMD’s financials, namely its revenue. The company experienced a 23% year-over-year revenue drop, which is expected to be mainly related to a drop in cryptocurrency prices. However, it has continued to improve its global margins significantly. Over the past year, the margins have improved from 36% to 41%. This is an exciting improvement to see for shareholders.

This has resulted in AMD continuing to earn respectable and growing income. I do look forward to the earnings stabilizing out as the company continues to improve its market position.

The company has used its earnings to improve its financial position respectably. Over the past year, AMD cut its debt by $165 million while improving its net receivable earnings by $155 million. This is an impressive one-year improvement in the company’s position, as it continues to invest in the viability of the long-term business plan.

As can be seen here, AMD’s financial position is continuing to improve. As the company continues to grow, this will drive additional rewards for shareholders.

Conclusion

AMD had a difficult time period from 2011 to 2016. However, the company is significantly improving its financial position, and continuing to invest heavily in its business. As a result, it’s continuing to gain against its competitors, especially Intel, which due to manufacturing problems, has been left behind.

Going forward, I recommend investing in AMD due to its impressive long-term potential to reward shareholders.

Disclosure: I am/we are long AMD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.